What is Break-even Point?

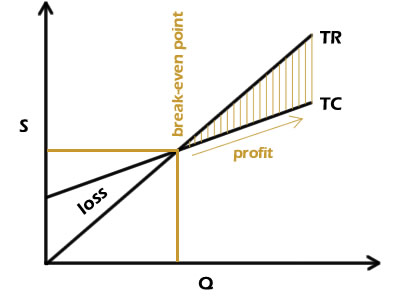

The break-even point is when the revenues of a company enable it to cover its costs. At this stage, the company manages to keep the business running, but does not yield a profit. The break-even point determines the number of products or the amount of sales that enables the business to break even. In order to break even, a business has to cover its fixed costs.

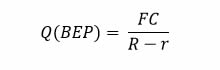

With the average price per product (R) and the average fixed cost per product (r), we can determine the quantity of goods that have to be sold in order to reach the break-even point. The following formula can be used to determine the quantity at break-even point (Q):

Sales at break-even point

The break-even point can also be determined based on the amount of sales. In that case, fist the sales revenue has to cover variable costs, then the fixed costs. Depending on the information at hand, the following formulas determine sales at break-even point (S).

This information is valuable to a business since it informs them about the point where they can manage to keep working. It also informs them that any quantity of products or amount of sales higher than this number lead to profit. Any less than that puts the business in jeopardy since even business costs cannot be paid. This means that the capital that was invested into the company has to cover for the expenses instead of being used to create a profit.

In certain cases, a business may indicate loss for some time, however, they are expected to break even at a certain point by gradually growing sales and eventually indicating profits that cover for those losses. Nonetheless, if a company’s losses become so high that they significantly damage business capital, in a short amount of time there will not be enough capital to produce products or offer services.

from breaking even to making profit

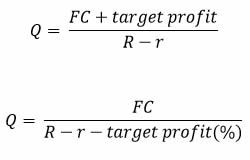

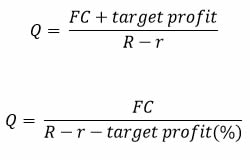

The same information can allow a company to determine the point where they can arrive at a desired profit. The general rule sates that total profit equals total revenue less total costs.

TP = TR – TC

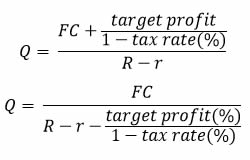

Since the break-even point is where revenues equal expenses, any number of products sold above that increases profits. Therefore, using the same information, we can determine the goal that leads the business to its intended profit. The expected or target profit is the amount that has to be reached in addition to the break-even point. The amount of target profit has to be included as the numerator. However, if you wish to determine the target profit based on a certain percentage, that percentage must be added to the denominator. Therefore:

The two last formulas above indicate a profit before tax. In order to reach a desired net profit, taxa rate has to be included as a variable as well. The formulas are the same, only tax rate is deducted from each target profit:

Break-even points help businesses plan and adjust their activities to reach a desired profit. They inform companies about the situation in which they are, and provide information based on which businesses can make sound decisions.